1. Income Tax on Interest

Any interest earned on your investment is included in your gross income for that particular tax year, even if you have re-invested the interest. This means it forms part of your income and will be taxed according to your income tax rate.

You do, however, qualify for an interest exemption, so you will not pay income tax on the first R23 800 of interest if you are under the age of 65, or R34 500 if you are over 65.

For example, if you had R400 000 invested in a money market account earning 5%, you would earn R20 000 in interest per year, which is below the taxable amount and no tax would apply.

2. Dividends Tax

Dividends tax is also payable each year on the dividends you receive as a natural person, even if your dividends are re-invested. The company that declares the dividend of the fund is responsible for withholding and paying the dividends tax to SARS. Dividend Withholding Tax (DWT) is levied at 15% on the dividends earned by an investor, but may be reduced if you are subject to a Double Taxation Agreement. Even though you don’t pay dividends tax yourself, you should disclose your dividends in your personal tax return.

3. Capital Gains Tax

Capital gains are taxed very differently to interest and dividends, as you only pay tax when you dispose of the asset – in other words, when you sell it. In the context of a financial asset, the growth on capital normally comprises the movement in price of the asset over a particular period of time. As the price of the asset increases, so does the capital appreciation of the asset, which in this case may be a unit trust fund or a share for example. Capital Gains Tax (CGT) is levied on the capital gain that arises on disposal. This is the difference between what the investor sells the asset for (“proceeds”) and what the investor acquired the asset for (“the base cost”). This means whenever units/shares are sold, either to be re-invested or withdrawn, a capital gains event will be triggered.

Natural persons and some special trusts are eligible for a CGT exemption of R30 000 per year, which reduces the impact of the potential tax payable by the investor. Only capital gains over R30 000 will be subject to CGT.

CGT is calculated based on your marginal tax rate. A third of the capital gain (33,33%) is included in your gross income for that specific year and taxed at your marginal rate.

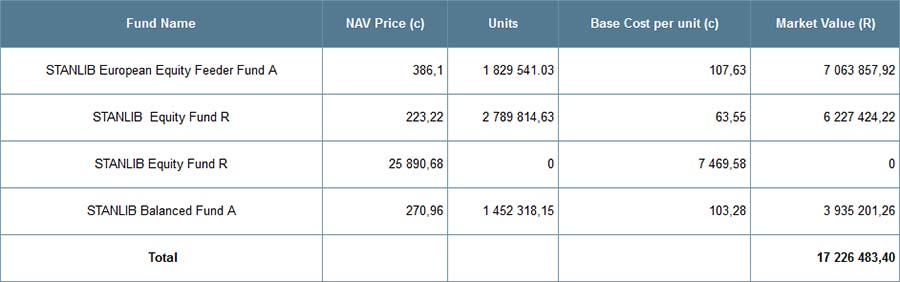

Fund Name |

NAV Price (c) |

Units |

Base Cost per unit (c) |

Market Value (R) |

STANLIB European Equity Feeder Fund A |

386,1 |

1 829 541.03 |

107,63 |

7 063 857,92 |

STANLIB Equity Fund R |

223,22 |

2 789 814,63 |

63,55 |

6 227 424,22 |

STANLIB Equity Fund R |

25 890,68 |

0 |

7 469,58 |

0 |

STANLIB Balanced Fund A |

270,96 |

1 452 318,15 |

103,28 |

3 935 201,26 |

Total |

|

|

|

17 226 483,40 |

Example

Below is an example of a STANLIB unrealised CGT statement. In other words, the money is still invested.

(A 41% marginal tax rate is used in the below examples)

In this example, the unrealised capital gain is R5 242 016 (R17 226 483.40 – units* base cost per unit).

If the client withdraws/switches their entire investment, then a capital gain of R5 242 016 would be realised and tax would apply.

If only a portion of the investment is realised, then the capital gain will realise on that particular portion.

The tax calculation:

R5 242 016,40-R30 000 (tax exemption) = R5 212 016,40

A third (33,3%) of the gain will be included in the investor’s taxable income when calculating the tax:

R5 242 016,40 x 33,33% = R1 737 165,07

This amount will then be taxed at the client’s marginal tax rate. (Assuming tax is applied at a flat rate of 41% without taking rebates into account.)

R1 737 165,07 x 41%

= R712 237,68 (potential tax to be paid)

CGT and Your Investment:

- A capital gain is not realised when transferring units of the same fund and class to another investment platform.

- A CGT event is triggered when an investment is transferred between different entities (natural person and trust for example).

- Retirement funds such as a Retirement Annuity, Preservation Fund, Pension or Provident funds are not liable for CGT. Nor are tax-free savings accounts.

- Capital gains are realised upon death. The CGT exemption upon death increases to R300 000.

- A capital gain does not arise when an investment is transferred to a spouse. However, the base cost will roll over to the spouse and he/she will be liable for CGT when they dispose of the investment.

|