Liberty recently launched a new innovative living annuity called Bold to help remove the sting of any market downturns.

Living annuities are a popular option for retirees as they offer income flexibility and the potential to outperform inflation, as well as the opportunity to leave an inheritance.

The challenge, however, is that a living annuity (which invests in funds with high-equity content in order to provide above-inflation growth) is at risk of market volatility, including market losses. Volatility not only affects the value of the capital invested, but also potentially the rand value of a retiree’s monthly income.

To avoid the worst of any market dips, some retirees go for a more conservative portfolio of funds with their living annuity, which offers lower market exposure, but also lower expected returns. Because of this, customers’ investment choices in retirement are often too conservative, resulting in returns that don’t keep up with inflation. Our research shows that many retirees are in danger of underperforming the fixed life annuity alternative, negating the benefits of a living annuity.

In order to provide our living annuity customers with the benefits of the higher-performing funds without all the extra return risks, Liberty has launched Bold – a living annuity that allows total flexibility in choice of funds at all times, but provides a Liberty return guarantee that increases as a customer’s returns increase.

How does this work?

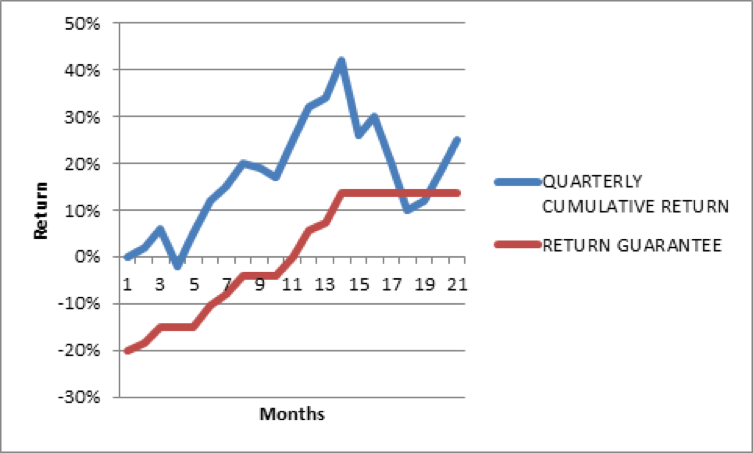

An investor can select any mix of underlying funds from a range of asset managers and change this at any time. Overlaid on top of this is the rising Liberty return guarantee, which is called an 80% high-water mark guarantee. This means Bold will assess the cumulative return the funds selected by the customer have delivered and whenever a new return high is achieved, the quarterly high-water mark and the guarantee will be set at 80% of that high.

On day one, the funds selected obviously have yet to produce any return and so the initial Liberty return guarantee is -20%. But, as soon as the selection of funds delivers a positive return at the end of any quarter, this guarantee rises. For example, if during the very first quarter the return from the underlying funds was 5% in aggregate, then the high-water mark and the guarantee would increase by 4% (80% of 5%) from -20% to -16%.

This means that if your cumulative aggregate return reaches 25%, then the high-water mark guarantee would have increased by 20% (80% of 25%) – from -20% to 0%. The return guarantee applies both to income withdrawals and the five-year point so at this point one would have the comfort of knowing that income withdrawals could never mean selling one’s capital to fund income at a negative return and that at the five-year point returns could not be negative either.

The quarterly high-water mark never reduces so right from the start of your investment your capital could never depreciate by more than 20%. Each quarter, 80% of any growth on the investment is effectively locked in, so if you had a negative quarter, the previous high-water mark would remain.

As Liberty Two Degrees is a REIT, it’ll be allowed to borrow money to invest in new properties. This gearing allows the fund to grow, but also increases the risk of the fund. Over time, the gearing should allow the LREP to increase in value ahead of the Liberty Property Portfolio, but at a higher risk. For investors who prefer less risk and a more predictable growth rate, the Liberty Property Portfolio would be more appropriate.

A unique charging structure

A rising return guarantee is very valuable, especially as it applies both to income withdrawals during the five-year guarantee period (whatever their level) and the five-year point. With Bold, you really only pay for the guarantee if the high-water mark rises. This is because although there’s a once-off charge, it’s just 1% on the first day of the investment and further charges only apply when an investor’s aggregate return exceeds 14% in any year. If it does, then at the end of the year we deduct 20% of any growth in excess of the 14% for the guarantee. For example, if the aggregate return is 20%, then a fee of 20% on the 6% above 14% would apply – therefore 1,20%.

Investors can switch off the guarantee at any time. When they do, if their return that year doesn’t exceed 14%, then they pay nothing (if it does exceed, then they pay 20% of the excess upon exiting the guarantee). This means full flexibility is maintained and investors only really pay for the performance guarantee once it becomes particularly valuable.

For more info, consult a Liberty Financial Adviser or broker.

Illustration

|