As a family you need to decide where a good education fits in your priorities. Sometimes it will come down to a decision between a new car and your child’s education.

When starting a savings plan for your children’s education, you need to be realistic about what your goals are. It would be very difficult to save enough money during your child’s first seven years that would be adequate to completely pay for their 12 years of school fees. Rather focus on meeting the gap between school fee increases and your salary increases, and to pay for those extras like books and school tours.

It’s likely that school fees will increase by more than your salary each year. Education costs have risen by between 9% and 10% each year, but salary increases have not matched this figure.

EDUCATION COSTS AS A PERCENTAGE OF INCOME

If you earned R10 000 a month in 1990 and spent R500 a month on your child’s education, you would have been spending 5% of your income on education.

If your salary only increased in line with inflation you would be earning R44 000 today, however, the cost of providing your child with the same education would have increased to R7 400 per month which makes up 17% of your income. This means that the amount you spend on education relative to your income has tripled!

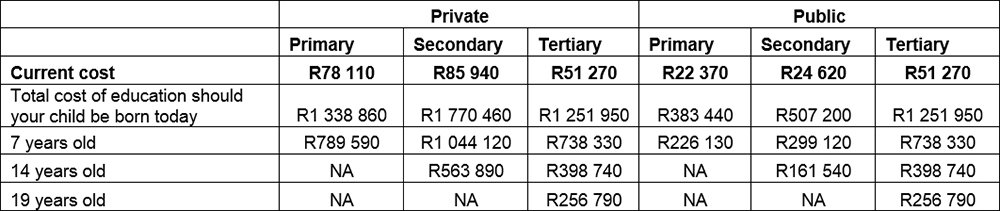

WHAT YOUR CHILD'S EDUCATION WILL COST YOU PER ANNUM BASED ON THEIR CURRENT AGE

If, for example, you've just had a child and intend on sending him/her to a public primary school, a private high school and four years of tertiary education you can expect to spend around R3.4 million on education – although keep in mind that this figure includes inflation so your salary would have more than doubled over that period.

WHERE SHOULD I INVEST FOR EDUCATION

Before you start saving, the first question you need to ask is “How long will I put this money away for?” Once you know how long you are saving for, you are able to select the correct savings vehicle.

Short term: If you’re saving just to pay for next year’s school books, invest in a product that will protect your capital. Any investment of two years or less should be in a high-interest bank account, money market fund or retail bond.

Longer term: If you’re saving for your child’s school fees in five years’ time or longer, you’ll need an investment that can keep up with inflation. The only way to ensure your child’s education fund keeps up with inflation is to invest in growth assets – namely shares on the JSE. You can do this through market related investments such as unit trusts or education plans that invest in growth assets. |